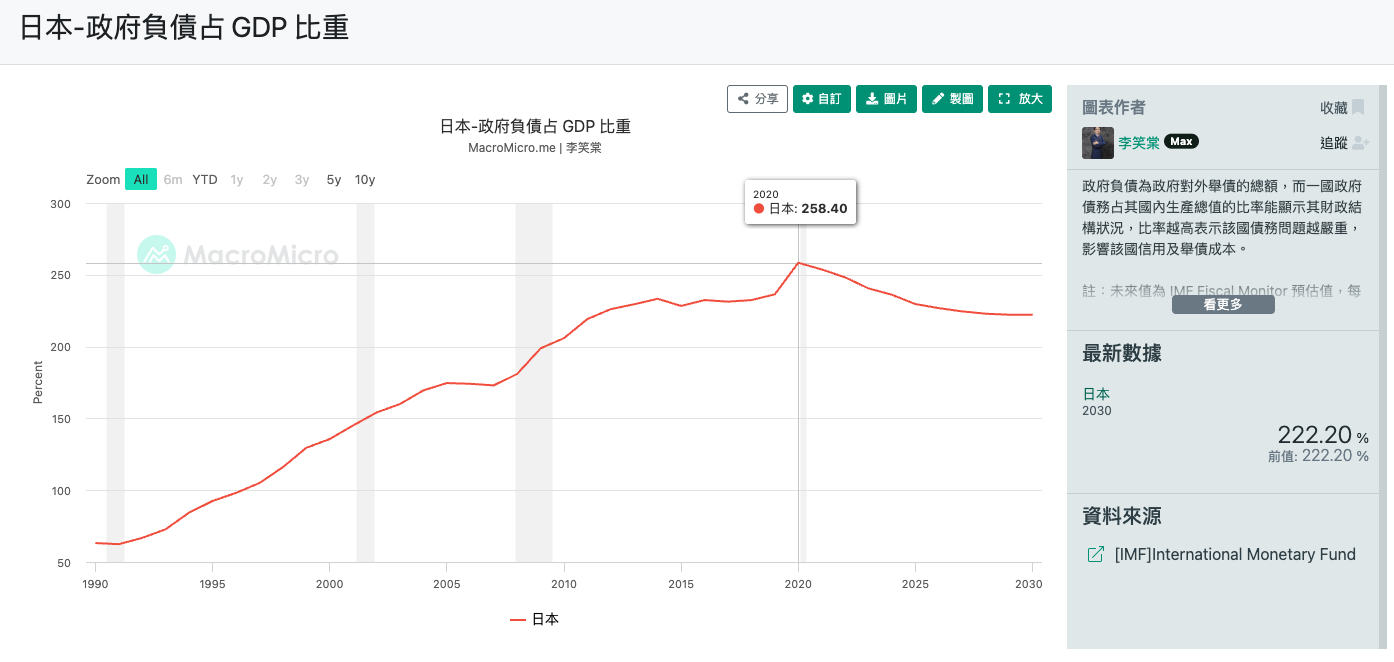

Why Japan’s debt-to-GDP ratio was 258.4% in 2020 but it hasn’t gone bankrupt? Why the Yen keeps falling, yet the government dares not hike rates significantly to save the exchange rate?

In early 2026, Japan is at a critical moment of “lifestyle shift”, moving from 30 years of “zero interest rates and deflation” to an era of “tangible interest and inflation”.

Behind all this points to the extremely contradictory relationship between “Government Bonds” and the “Yen”.

Why keep borrowing when debt is piling up?

Many people’s first reaction to Japan’s astonishing debt ratio is:

Why hasn’t this country collapsed yet?

In reality, the Japanese government is now “forced to issue bonds”, with the following core logic:

| Reason | Explanation |

|---|---|

| Rigid Demand from Aging | Medical and pension expenses grow automatically, and this money cannot be saved. |

| Debt Snowball | Much of the current bond issuance is for “borrowing new to repay old” (refinancing), and debt service costs already take up 1/4 of the government budget. |

| “Left Hand to Right Hand” Structure | Half of the national debt is held by the Bank of Japan (BOJ), so interest circles back to the government; most of the rest is held by domestic institutions, giving Japan strong resistance to external risks. |

| Addiction to Low Rates | Long-term ultra-low interest rates have given the government an illusion of “debt is not a worry”. |

| Aggressive Fiscal Route | The government tends to pursue nominal GDP growth through investments (e.g., defense, semiconductors, digital development), which also requires money. |

Simply put, Japan is now like being on a treadmill that cannot stop, and can only keep running.

How do Government Bonds “Kidnap” the Yen?

So what does this have to do with Yen depreciation? This is the so-called “Love-Hate Relationship” mechanism.

Because Japan owes so much debt, the Bank of Japan's (BOJ) room for interest rate hikes is very limited.

If interest rates rise too fast, the interest on government bonds the government has to pay will explode, and finances will collapse instantly.

This creates a vicious cycle:

| Result | Explanation |

|---|---|

| Dare not hike rates | Worry about widening interest rate spread between Yen and USD, capital outflow, and continued Yen depreciation. |

| Depreciation triggers inflation | Imported energy and food become expensive, causing public grievances. |

| Handing out subsidies | To appease the public, the government has to distribute money to subsidize electricity bills or give cash. |

| Issuing more new bonds | Where does the subsidy money come from? Only by issuing more bonds. |

As a result, the scale of government bonds becomes larger, and the central bank dares not hike rates significantly. The Yen is thus “kidnapped” by its own massive debt.

Real Challenges and Public Pain Points in 2026

How does this macroeconomic wrestling translate into pressure for ordinary people?

1. Mortgage Holders: “Boiling Frogs”

If you have a floating-rate mortgage, you might be facing danger now. Although Japan has the so-called “5-Year Rule” (monthly payments unchanged for five years), this is just delaying the pain.

When interest rates rise, although your monthly payment hasn’t changed, the “interest portion” inside it has increased. If rates rise high enough, a situation where “monthly payment is not enough to cover interest” might even occur, which is called “unpaid interest”, and it will accumulate on your principal.

2. Getting Poorer Without Investing

In the past, Japanese people thought saving money was a virtue, but in 2026, bank interest rates are far behind inflation. This is also why the government is vigorously promoting the NISA (Nippon Individual Savings Account) system.

If you don’t learn to manage finances, your assets will be slowly eaten away by inflation.

3. The Last Straw: Shunto

The “Shunto” (Spring Wage Negotiations) in 2026 is crucial. If the wage increase loses to inflation plus interest rate increase, then the financial crisis of the middle class might officially detonate.

Conclusion and Outlook

The Japanese government is currently walking a tightrope, trying to use “minor rate hikes” to buy a little dignity for the Yen, while also using “bond issuance subsidies” to maintain social stability.

For us, understanding this situation allows us to understand why we must switch from “Saving Mode” to “Investment Mode” now. 2026 is not the end of turmoil, but the beginning of a new era.